http://seekingalpha.com/article/267950-ipath-s-p-500-vix-short-term-futures-etn-swimming-against-the-currents

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

The VIX volatility index has made headlines in recent weeks by remaining at relatively low levels despite the great many potential catalysts for market upheaval. Many contrarian-minded speculators have been enticed into going long volatility -- and an increasingly popular way to accomplish this is with the VXX.

What investors in VXX must know is that the odds of profiting are not all that different from a video poker machine and the ETN administrators have about as much to gain from this as a Las Vegas casino.

Background

First, a quick primer on the VXX. VXX is an iPath ETN designed to mimic a 30 day futures contract on the VIX spot index (note: the VIX "spot" index is not directly tradable, so short term futures are the nearest proxy). The fund managers accomplish this by maintaining a balance of front-month (the next futures expiry date) and second-month contracts that keep the VXX always about 30 days out on the curve. As an example, on T=1, the first day after contract expiry (e.g., May 18), the VXX "holds" only contracts for the next expiry (June contracts). By T=15, the VXX consists of 50% June contracts and 50% July contracts, thus maintaining the 30 days away from expiry structure. Therefore, each day the VXX "sells" 1/30th of its assets in front month contracts and rolls them into second month contracts.

Pretty clever. However, there's a big catch. When the VIX futures curve is upward sloping, meaning people expect volatility to be greater in 2 months than in 1 month and so forth, there's an ongoing premium that must be paid to continually sell front month contracts and replace them with second month contracts (which, themselves, become front month contracts in a few weeks' time). This situation of more distant futures costing more than near-term ones is referred to as contango and the buy-high-sell-low situation it creates is called roll yield. VXX mirrors exactly this strategy, as is clearly laid out in the prospectus.

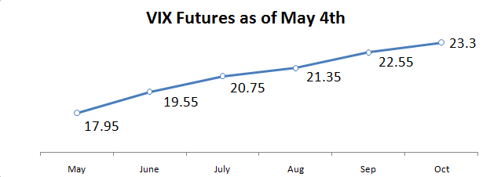

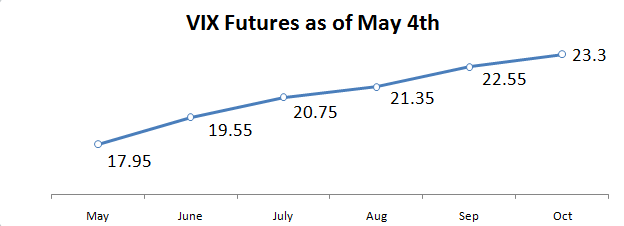

Recent impact as of this writing, the VIX futures curve looks as shown below. All else being equal (i.e, no shifting of the curve), if you buy a June settlement contract today and hold it for a month, you can expect that it'll trade at a price similar to what the May contract is at today. In other words you'd buy at 19.55 and in a month it would be worth 17.95, a roll yield of about 8%, which is analogous to paying an 8% monthlypremium to maintain a front month portfolio.

(Click to enlarge)

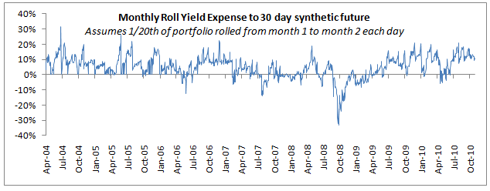

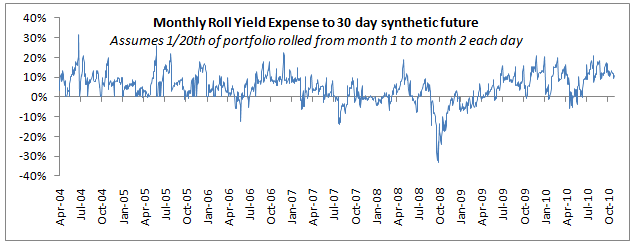

One interpretation is that the market is simply anticipating a rise in volatility in the next couple of months. However, here's the wrinkle: the VIX futures curve has been upward sloping (in contango) for the front two months about 75% of the time. The below chart shows the monthlyroll yield impact for the front month to second month from 2004 to 2010. Note, the below data was manually assembled from multiple source files on the CBOE website and may contain some errors.

(Click to enlarge)

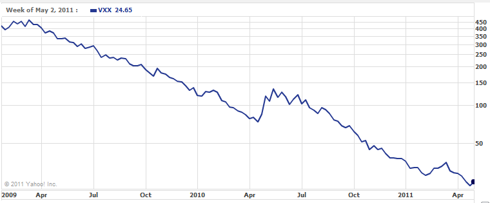

Of course, paying a 5% or 10% or 15% monthly roll yield is a huge headwind for the VXX, and not surprisingly it has lost almost 95% of its value since its launch just 25 months ago. With the logarithmic Y axis, the constant decay nature of the VXX is strikingly apparent.

(Click to enlarge)

A Theory…

So, the empirical evidence isn't favoring investment in the VXX, but perhaps longs are "not wrong, just early" as the saying goes? Is the market simply anticipating an increase in spot volatility that will eventually vindicate the VXX holders and cause a regime change from contango to backwardation?

Don't bet on it. According to Yahoo Finance as of this writing, VXX has assets of about $1.44B, suggesting exposure of somewhere between 0 and 1.44B in front month futures and the remainder in second month contracts. Assuming 21 trading days in a month, this implies that somewhere around $68M of month 1 contracts must be rolled into month 2 contracts every day. Based on the past couple weeks of market data, the May and June contracts (current M1 and M2) are trading around $200M to $300M per day, implying that the VXX daily rolling is already becoming 20-30% of the futures market volume, a huge number.

Since the buying and selling of transactions are always in the direction of steepening the futures curve (selling M1 contracts pushing down the futures price of M1, buying M2 contracts, lifting the futures price of M2) the VXX itself may become a structural reason for the very contango that is destroying shareholder value.

It's important to note, however, that VXX is an ETN, which differs in an important way from an ETF. While an ETF claims to hold a portfolio of the actual assets on which the fund is priced, an ETN is a simple promise to pay out based on a certain formula applied to traded instruments.

Thus, it's quite possible that Barclay's/iPath does not hedge their risk exposure, or hedges only partially. In an inquiry to their Investor Relations department, iPath provided the following disclosure:

Since iPath ETNs are unsecured debt instruments issued by Barclays Bank PLC, there are no assets to secure these products. The iPath ETNs simply pledge the returns of the index less the investor fees. For these reasons, the information on how the assets are invested is not disclosed.

Given the structural flaws of VXX, I wouldn't blame iPath if they chose not to hedge, and instead chose to effectively remain short the instrument they created. If that's the case (and I have no way of knowing), I would find it unsettling to have my interests in direct opposition to the creators of it. It would be like investing with a fund that received a performance bonus on losses.

If I were long VXX, I'm not sure which would be more unsettling: knowing that the fund's hedging was moving the markets into contango or the that the instrument's sponsor was betting on its continued decline. Since the VXX continues to gain in popularity and size, I suspect that whatever is happening will not relent.

The Trade

This is the easy part. Stay away from the VXX, or if you have the stomach, short it. The trick, of course, is that volatility can be volatile. Being too aggressive with shorting a contract that can spike so abruptly is a bad idea, no matter how favorable the odds. Prudent risk management practices of limiting the position to a small fraction of your portfolio and setting a worst case stop loss (either real or mental) can keep the downside manageable.